[ad_1]

Like many things surrounding the blockchain community, Ethereum’s smart contracts can be a confusing concept to most.

Smart contracts seem a bit difficult to understand because the term confuses the base interaction described. They are a new possibility due to the ethereum public blockchain.

A smart contract binds a relationship with cryptographic code, whereas a standard contract is an outline of the terms of a “relationship” and is usually enforced by law.

To describe them a little more clearly, smart contracts are programs that carry out the exact tasks set by their original makers. They help you exchange money, shares, or anything of value in a conflict-free way while staying away from the needs of a middleman.

Nick Szabo a cryptographer and computer scientist, first developed the idea back in 1993 and had the idea of it being a ‘digital’ vending machine. In a simple example, you drop 10 ether into a ‘vending machine’ (i.e. ledger), and your driver’s license or escrow drops into your account. Smart contracts automatically enforce and define the rules/penalties around the agreement originally created. Ethereum’s platform is built specifically to create these smart contracts.

These tools aren’t meant to used in seclusion but are meant to shape the building blocks for the decentralized applications and decentralized autonomous companies described in our previous articles.

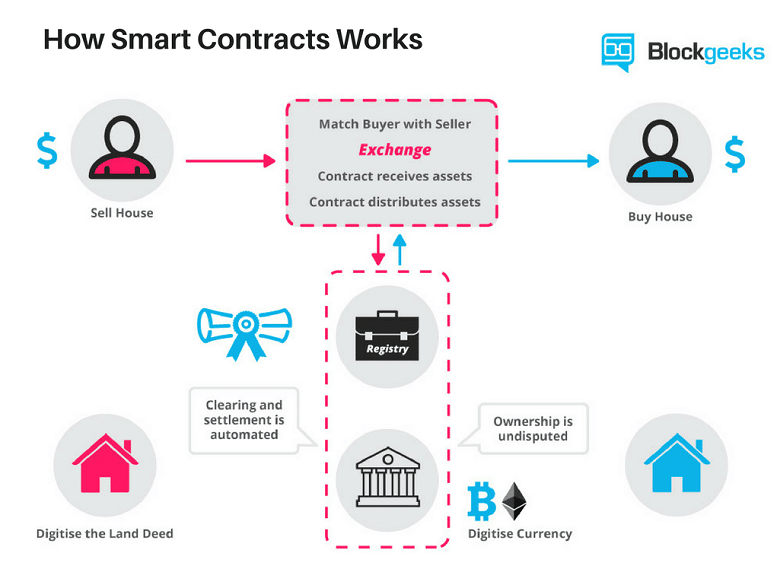

How do these “smart contracts” work?

Contracts can be encoded on any blockchain and Bitcoin was the first to support the most basic of smart contracts. It was the transferring of value from one person to another but it is very limited to the currency use case.

Instead, ethereum replaces bitcoin’s limited ‘language’ and succeeds it with a language that grants the developers opportunity to write their own programs.

Ethereum’s ‘turing-complete’ supports a wider set of computational instructions and allows developers to program their own smart contracts.

Smart contracts provide:

- Autonomy – The originator of the contract is the primary executor of the agreement. You don’t need to rely on a lawyer or a broker and it knocks out the dangers of error or corruption from the third party.

- Trust – Your information is encrypted and stored on a shared ledger, there is no way it can be “lost.” With that, it’s also backed up with all the nodes in the network storing your data.

- Safety – Cryptography, the encryption of websites, keeps your information safe and it would take an abnormally high skilled and wealthy hacker to infiltrate the system.

- Speed – Without the need of paper and having to manually construct each contract, it presents the opportunity for businesses to save time and money.

- Savings – As just previously stated about businesses saving money with these contracts, individuals are able to save on notary/lawyer fees that occur when someone is needed to witness or process your transactions.

- Accuracy – Instead of having to fill out piles of paperwork with a larger margin for error, automated contracts avoid those errors.

Blockchains That Are Able To Process Smart Contracts:

- Bitcoin – Excellent for processing Bitcoin transactions but limited processing documents.

- Side Chains – Block Chains that run adjacent to Bitcoin and offer a bit more for actually processing contracts.

- NXT – Public blockchain that provides a few choices of smart contract templates. You are unable to code your own contracts.

- Ethereum – Public blockchain that allows complete freedom with coding and implementation of smart contracts but you are responsible for the computing power with “ETH” tokens.

Featured Image: twitter

[ad_2]

Source link