- The Bitcoin New York Agreement was a memorandum of understanding signed by 58 Bitcoin companies aimed at solving Bitcoin’s scaling issues

- The meeting to thrash out the details of the agreement was held ahead of the 2017 Consensus conference

- The agreement was supposed to raise Bitcoin’s block size to 2MB, but it was dead within six months

The Bitcoin New York Agreement was an agreement drawn up in May 2017 following a multi-day meeting with 58 of the top Bitcoin companies in the world at the time with the intention of solving Bitcoin’s scaling problem. The resulting agreement would have been the first stepping stone on the path to a cheaper Bitcoin, but less than six months later it was dead in the water. So what was the Bitcoin New York Agreement all about and why did it die?

The Background

Bitcoin’s scaling debate had been rumbling since 2011 when the limitations on the 1MB block size cap, implemented at the last minute by Satoshi Nakamoto prior to Bitcoin’s launch in 2009, were becoming evident – with increasing popularity and usage, the Bitcoin blockchain would clog up and transactions would become both slow and expensive.

Several solutions had been discussed by miners and developers in the intervening years, including two forks (Bitcoin XT and Bitcoin Classic) and the discussion of a soft fork called SegWit, which would go some way to alleviating the pressure on the blockchain. This didn’t appease those who wanted bigger blocks however, and no proposal gained more than 40% of support from miners.

With many parties due to be present at Consensus in 2017, clear-the-air talks were planned ahead of the conference itself with the idea of coming to a comprehensive agreement about how to scale Bitcoin in a manner that pleased everyone just enough to not argue any further about it.

The Meeting

Representatives from over 50 companies attended the meeting, including developers, miners, and the heads of leading Bitcoin companies, which took place around the weekend of the 20-21 May. There was obviously plenty of bad blood in the room, with Bitcoin company Blockstream, which employed several of the key Bitcoin developers, accused of having a financial incentive to keep the block size low, including owning patents surrounding the SegWit code and the Lightning Network, which implementation of SegWit would allow.

However, Blockstream CEO Adam Back had declined to attend the meeting and there were no other Blockstream representatives there to debate these issues, an omission that would be telling down the line.

The ramifications of block size increases were discussed, with ‘big blockers’ pointing out that maintaining a low block size would kneecap Bitcoin’s potential and increase the transaction fees, while ‘small blockers’ pointed to a potentially spiralling blockchain size making running nodes impractical. Interestingly, both sides have since claimed that their visions represent Satoshi Nakamoto’s original vision, which is testament to the lack of clarity the man himself offered on the matter.

We don’t know too much of what was actually said at the meeting, but what we do know is that the concept of the SegWit soft fork was raised as a potential middle ground. SegWit itself would act as a side chain to take some of the pressure off the main chain and would usher in the potential of the Lightning Network, which some argued was a Trojan horse implemented by Blockstream to get more of its software into general use.

Middle ground was eventually found on the SegWit front, but only if a block size increase to 2MB blocks would follow. This was decided as the best compromise for all parties, and with the signatories representing over 80% of the global Bitcoin mining hashrate it was almost certain to be accepted once submitted to the network. At last, Bitcoin could scale.

The Agreement

The Digital Currency group posted details about the agreement on May 23:

This agreement was met with a sigh of relief throughout the Bitcoin community, with the promise from all sides to commit to “the research and development of technical mechanisms to improve signaling in the bitcoin community, as well as to put in place communication tools, in order to more closely coordinate with ecosystem participants in the design, integration, and deployment of safe solutions that increase bitcoin capacity.”

As a result, everybody connected to the Bitcoin ecosystem began working on preparing their software for the Segwit2X upgrade. Or at least, almost everybody.

The Lead Up

SegWit was locked into the Bitcoin code in June 2017, with a go-live date of early August, meaning that the block size increase would theoretically be implemented around Christmas Day. This confirmation went down particularly badly with a certain set of big blockers, among them Roger Ver and Craig Wright, who set about creating a hard fork of Bitcoin in response, which would have an 8MB block size by default, with further increases planned in the future. Bitcoin forked into Bitcoin and Bitcoin Cash on August 1, with SegWit activating seven days later.

Not long after this however, the 2x part of SegWit 2x looked to be in trouble, with Cointelegraph reporting that “The New York Agreement appears to be crumbling”. Faced with the very real prospect of Blockstream’s Bitcoin coders not implementing the block size increase given that they hadn’t signed the agreement, signatories began backing out of the New York Agreement, including major mining pools, whose agreement was critical to its implementation.

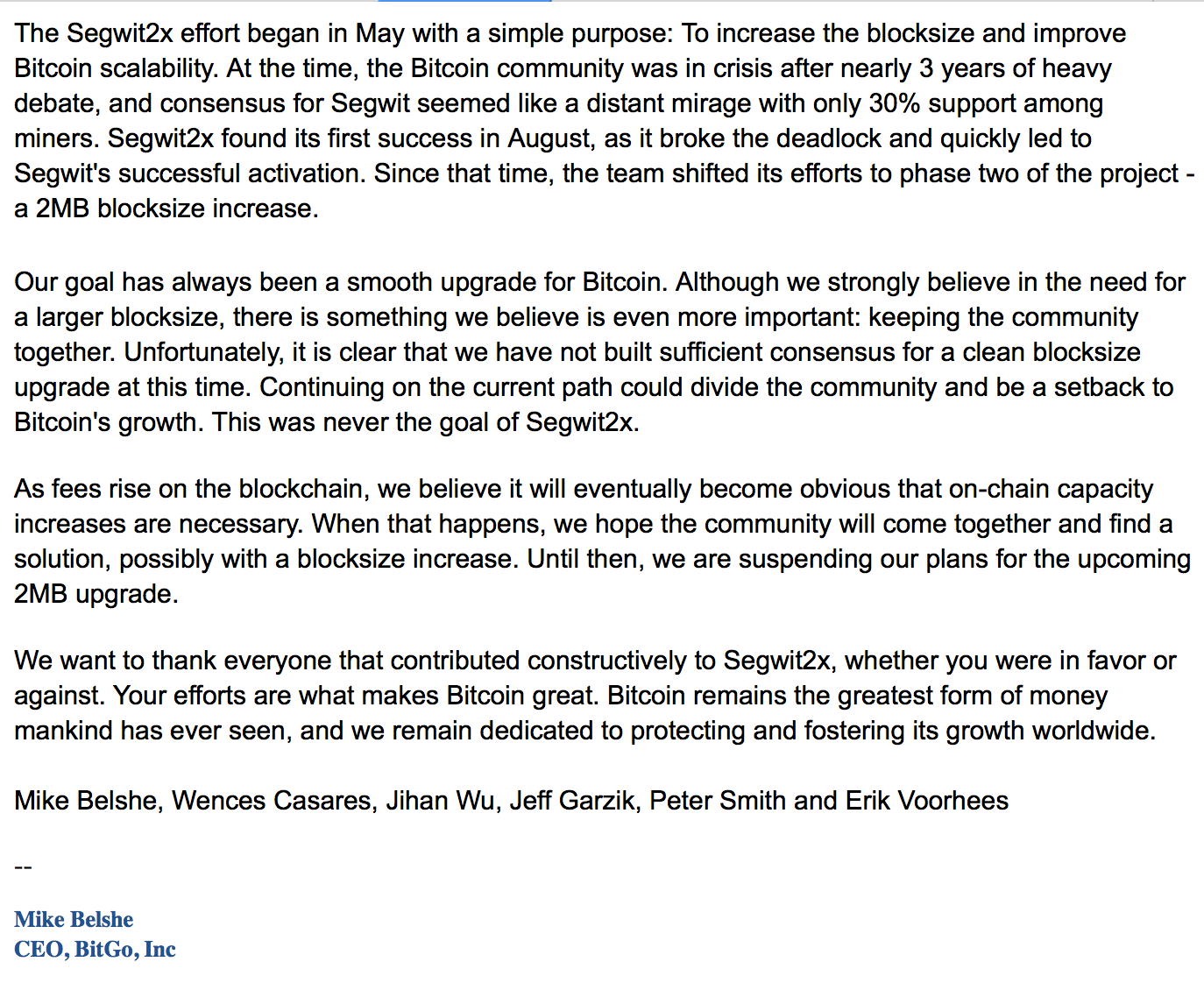

Despite this, by late October cryptocurrency exchanges and wallet markets were still preparing their customers for the changes that were about to take place, and Bitcoin looked set for its block increase. On November 8 however, all that changed:

Recognizing that the hard fork would no longer win the approval of miners (and perhaps knowing that Blockstream wouldn’t countenance the code change), these six individuals, who held positions of huge power and influence within their respective camps, called off the block size increase of SegWit2x. Incredibly, four days later, Blockstream CEO Adam Back said on Twitter that he would approve of a block size increase “probably [in the] mid term with testing”, a theory he could have pushed at the meeting had he chosen to attend instead of speaking after the plan was dead.

Recognizing that the hard fork would no longer win the approval of miners (and perhaps knowing that Blockstream wouldn’t countenance the code change), these six individuals, who held positions of huge power and influence within their respective camps, called off the block size increase of SegWit2x. Incredibly, four days later, Blockstream CEO Adam Back said on Twitter that he would approve of a block size increase “probably [in the] mid term with testing”, a theory he could have pushed at the meeting had he chosen to attend instead of speaking after the plan was dead.

The Aftermath

Bitcoin’s price collapsed from $7,500 to $5,800 on the news but soon recovered, while fees rocketed to $25 per transaction. Two weeks after the block size change was scrapped, Bitcoin developer Jimmy Song penned a blog post to explain that there were critical bugs in the code that would have killed the new chain anyway, so it was lucky it was never approved. Whether this would have come to pass or was just another excuse, only Song knows.

The scaling debate has never gone away, although it has become less fierce in more recent times. This is because those who advocated for the block size increase have either sold out and no longer discuss it, like Mike Hearn, or are focused on the forks that resulted from the debate, such as Roger Ver (Bitcoin Cash) and Craig Wright (Bitcoin SV).

Bitcoin transaction fees hit all time highs during the 2021 bull run at around $28 and currently sit at around $2. Another bull run will see the exact same thing happen again and there seems to be no further discussion over Bitcoin scaling on-chain. Meanwhile, virtually every block on the Bitcoin blockchain is at capacity, while the Lighting Network, which can thank its emergence to the activation of SegWit, has grown enormously, with almost 4,000 BTC committed to its channels.

Whether they intended it or not, the block size impasse has worked out well for Blockstream indeed.

Bitcoin New York Agreement Remains a Missed Opportunity

The Bitcoin New York Agreement wouldn’t have solved Bitcoin’s scaling problem had its agreements been fully implemented, but it would have been a start – a common ground from which the relevant parties could have worked to scale Bitcoin to meet its full potential. It remains a missed opportunity, with recriminations still thrown about and the ramifications still felt, and it may well represent the last time that almost all of Bitcoin’s warring factions came together to agree on something.